Perspectives on the Iranian conflict

Over the weekend, the conflict between Iran, Israel and the United States escalated significantly. A coordinated U.S-Israeli air and missile strike was executed inside Iran. Extensive attacks on military sites and command centres resulted in the confirmed death of Iran’s Supreme Leader Ayatollah Ali Khamenei. Tehran retaliated with missile and drone strikes against Israeli territory and U.S military bases across the Gulf region. The outcome so far has been casualties on all sides, disruption of regional air and shipping traffic, and fears of a widening regional war.

The outlook remains uncertain, particularly the timeframes for the conflict, and the extent of the impact on the global economy. Iran is likely to see this conflict as an existential threat, which increases the risk of a prolonged, broader conflict. We think the key economic flow on effect remains the impact on oil prices. But a wider impact on risk premiums is also likely to leave market volatility higher in the near-term.

What are the key economic risks?

Oil prices: Iran is a member of the oil producing cartel, OPEC. Iran’s production is likely to be disrupted by the conflict. A key risk to global supply is disruption in the Strait of Hormuz, through which around 20% of global oil trade passes. Iran has historically threatened but not enacted military disruption. Three ships have already been attacked near the Strait, and Iran has warned ships not to pass through. If the Strait is mined, then global oil supply could face months of supply disruption. Oil prices could move significantly higher from the recent tight range, representing a tax on households and a drag on economic growth.

Inflation: Inflation has proven sticky over recent months. We’ve identified two-sided risks to inflation over the medium-term. Meaningfully higher oil prices are a risk to global headline inflation. Central banks tend to look through spikes in inflation resulting from higher oil prices. We expect that to be the case for the US Federal Reserve, where core inflation ex-energy will remain the focus. Even so, higher headline inflation could delay the three rate cuts that are priced over the next twelve months. In Australia, the RBA already has a hiking bias. While the Bank will try to strip out the impact of oil, a prolonged period of inflation could add to pressure to hike sooner, or leave rates elevated for longer.

What are the key market risks?

Risk premiums: Equity market risk premiums have narrowed as valuations have surged towards record highs. Historically, periods of conflict have resulted in a short-term widening in risk premiums and elevated volatility. Given current elevated valuations, this risk is probably greater. But markets typically stabilise unless there is a sustained supply shock, which remains a key uncertainty. For now, we are concerned about elevated valuations and the risk of higher volatility.

Currency: The Australian dollar has recently strengthened as interest rate differentials have favoured the local currency. But we think the AUD remains a risk-sensitive currency. Energy spikes have also historically weighed on the AUD. Near-term, the AUD will likely face some downside risk but with the currency currently around USD0.70, we still see two-sided risk to the medium-term outlook. We continue to suggest that portfolios remain around their neutral hedge ratios.

Safe-havens: Historically, conflict has supported global safe-havens in the near-term. We expect gold and US Treasuries could attract flows in the near-term. Gold has rallied recently back towards record high levels which we suspect reflects safe-haven flows and inflationary concerns.

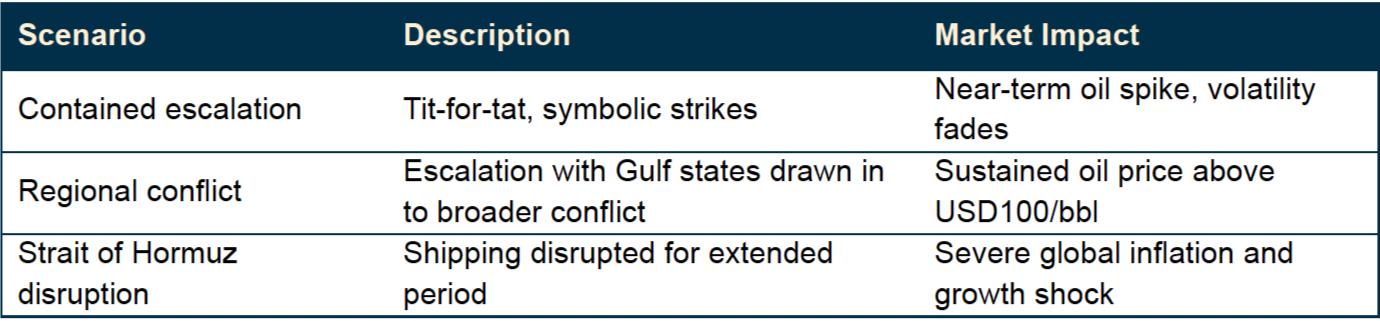

What are the escalation scenarios that we are monitoring?

The table below shows three potential scenarios we think could unfold. For now, our base case is contained escalation. But the risk of a regional conflict or prolonged disruption via the Strat of Hormuz increases the longer the conflict is drawn out.

Geopolitical risk and periods of conflict tend to drive volatility higher. But these periods have historically not lasted beyond the near-term. This current conflict could deliver a longer period of uncertainty if oil and energy prices climb higher for a prolonged period.

While this uncertainty persists, our focus will be on:

Reviewing diversification in portfolios and continuing to rebalance consistently.

Remain invested: Even though uncertainty is elevated, resist the temptation to move to cash and sit out the volatility. Trying to time the market is unlikely to deliver outcomes that achieve most investment objectives. Instead, remain invested and rely on diversification to help mitigate risk.

Review portfolio risk: The strong returns enjoyed over the past three years may have resulted in unintended risks within portfolios. This could include concentrations in one or more sectors or markets, higher risk exposures to certain types of credit, or sensitivity to certain macro drivers.

Stay close to longer-term strategic asset allocations: Elevated volatility and uncertainty may not adequately reward tilts away from strategic asset allocation.

We will keep you informed as the conflict develops and as always, if you have any questions or concerns please contact us.

Regards,

Derek & Leesa